Working in New York City with a rideshare app involves not only navigation and passenger handling, but also a steady routine around insurance paperwork. The city treats for-hire vehicles differently from personal cars, and coverage should reflect that usage every day, not just during trips. Searching for options like UBER insurance NYC often reveals a mix of personal, rideshare, and true for-hire policies, in most cases only one of these meets TLC rules consistently. For many, clarity arrives after understanding which documents are checked, who files them, and how renewals align with licensing deadlines. Details matter.

How TLC coverage fits daily driving

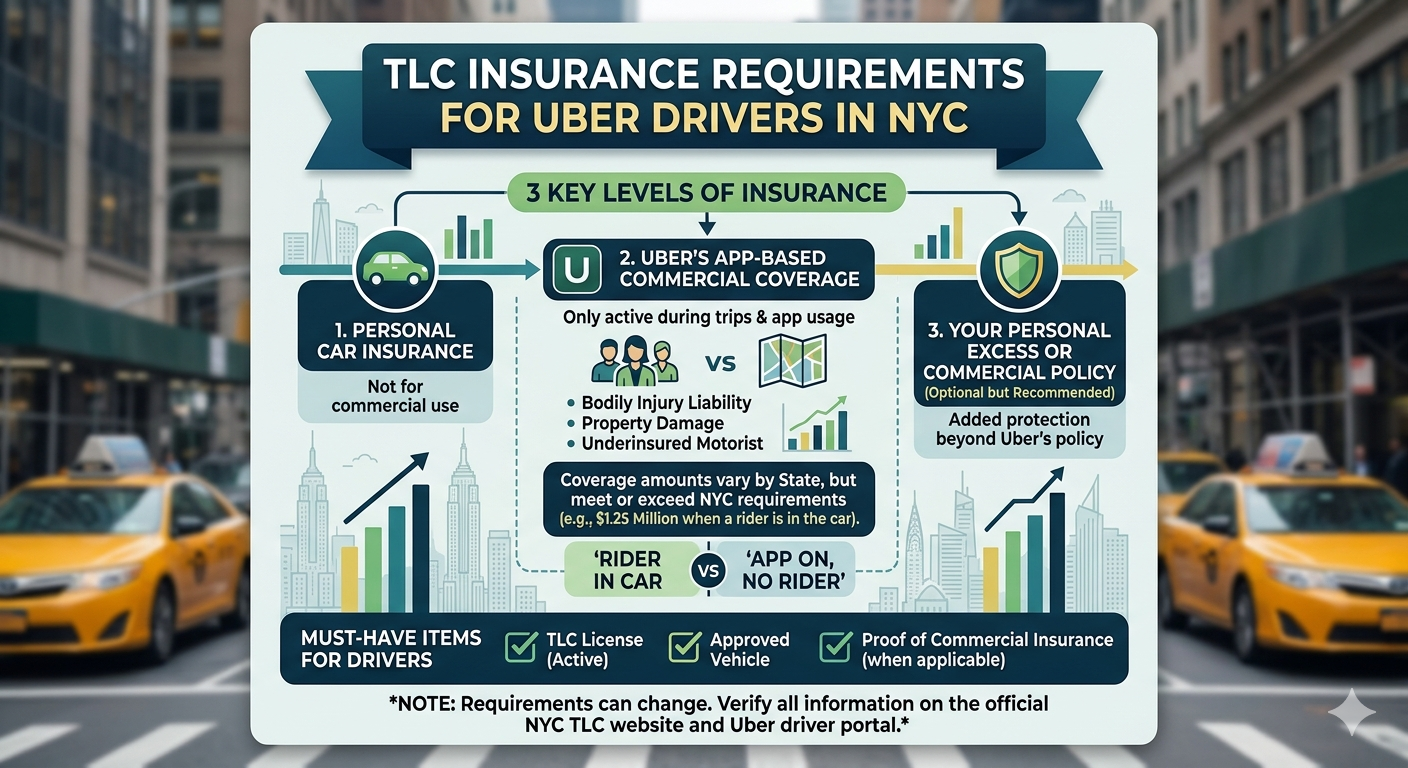

In practical terms, TLC‑compliant insurance is a commercial, for‑hire policy intended for continuous passenger‑carrying use within the city. It typically includes state no‑fault benefits under New York law, liability at TLC‑set minimums for for‑hire vehicles, and uninsured/underinsured motorist protection. Collision and comprehensive are optional from a regulatory point of view, yet often required by lenders or chosen to limit downtime after minor incidents. On the street, it becomes clear when a policy is tuned for heavy, stop‑and‑go city traffic.

Insurers and brokers sometimes reference this coverage as TLC insurance New York, distinguishing it from personal auto with a rideshare endorsement used elsewhere. The practical difference is that a rideshare add‑on usually activates only while the app is on, while TLC coverage assumes commercial use throughout the vehicle’s schedule. That assumption often affects underwriting, claims handling, and what proof authorities accept at inspections. In practice, inspection teams notice inconsistencies quickly.

Understanding documents, limits, and timelines

The day‑to‑day routine hinges on having the right papers ready and correctly filed:

- An insurance ID card and policy declarations naming the vehicle for for‑hire use, matching registration and licensing details.

- Electronic filings from the insurer to the DMV and the Taxi &, Limousine Commission confirming active coverage, many carriers submit these automatically.

- If a base or dispatch requires it, an additional insured or certificate holder entry, so operations proceed without administrative holds.

- Clear contact points for claims and endorsements, since vehicles in city service change plates, garaging addresses, or lienholders more often.

Timeframes matter. New policies or changes may take one to three business days to appear in agency systems, so starting early often helps. Binders can bridge brief gaps, but for many only official filings prevent lapses and potential suspensions. In practice, a small mismatch in a VIN or plate can delay activation longer than expected. Simple, but crucial.

Liability limits and no‑fault provisions merit periodic review, especially when vehicles are financed or dispatched by multiple bases. Small misalignments between declarations, registrations, and TLC records tend to surface during spot checks. The pattern repeats in busy weeks.

Weekly habits to keep policy compliant

- Check expiration dates for policy, TLC license, and inspection, aligning renewals to avoid midweek gaps.

- Confirm that documents show “for‑hire” or “livery” use, screenshots help if roadside verification is needed.

- After any address, plate, or base change, notify the insurer, then verify that agencies reflect the update.

- Track deductibles and roadside coverage, since quick repairs limit lost earnings after minor damage.

Treat UBER insurance NYC as a standing operating cost, not a project for the last renewal day. Small routines-calendar reminders, a scanned declarations page, and periodic confirmation that filings are current-often prevent disruption. Renewals for TLC insurance New York may also require fresh registration copies or driver license updates, so keeping a digital folder simplifies each cycle. During random checks or surprise audits, quiet preparation tends to reduce stress.

A steady insurance routine rarely looks dramatic, and that is the point. By focusing on clear documents, timely filings, and modest weekly checks, the vehicle stays eligible, dispatch remains open, and work continues without avoidable interruptions. The approach is simple enough to repeat and flexible enough to accommodate route changes, new vehicles, or shifting schedules.